The Ultimate Guide to a Credit Freeze

Being a victim of identity theft is an evil I wouldn’t wish upon my worst enemy. Here’s how a credit freeze has helped me keep my credit record in check, and how it can protect you too.

This post contains affiliate links, which means I may earn a small commission at no extra cost to you. For more information, please see my disclosure here. Thank you for your support!

Identity theft has become more and more common in the past several years. Decade or so ago thieves had to dig through your trash to get to your most private information. Nowadays, most data is just a few mouse clicks away.

According to the Identity Theft Resource Center, data breaches hit a record high of over 1,500 breaches in 2017. This exposed upwards of 14 million credit card numbers and 158 million social security numbers.

My data was compromised in one such breach. At first I didn’t pay much attention to it. Once I started seeing unauthorized charges on my credit card though, I took notice.

I immediately contacted my credit card company to report the fraudulent activity. Thankfully, their investigation concluded that I was not at fault. Although the fraud didn’t cost me anything this time, this wasn’t the first time my information was compromised.

I decided it was time to put my credit on lock. Today, I’d like to share with you everything I’ve learned about credit freezes through this process.

What’s a Credit Freeze?

A credit, or security freeze, is a tool that allows you to “lock” your credit report.

When you apply for credit, whether it’s a loan, a credit card, or a mortgage, the potential creditor will want to pull your credit report from one of the three Credit Bureaus to check on your credit worthiness.

If a thief steals your identity and wants to obtain credit in your name, they would have to go through the same process.

By locking your credit, the potential creditor will not be able to pull your credit report, and thus the credit request from the thief would be denied.

After placing a freeze on your credit, if you want a creditor to check your credit, you’d have to lift the freeze temporarily to give the creditor access to pull your report. For example if you’re applying for new credit or are looking to rent.

If you’re no longer concerned about security issues, you can always lift the freeze permanently from your credit.

Related Posts:

The Beginner’s Guide to How Credit Scores Work

6 Mistakes that are Killing Your Credit Score

How to Get Your Credit Score Up By 300+ Points in 5 Proven Steps

What are the Pros and Cons of Having a Credit Freeze?

As with anything, requesting a credit freeze has its pros and cons. Here’s some that you should consider before locking up your credit reports.

Pros

A credit freeze can protect you from thieves opening new lines of credit

Requesting a credit freeze does NOT affect your credit score

You can add, remove, or temporarily lift a credit freeze at any time for free

Cons

A credit freeze will NOT protect thieves from accessing your existing accounts without your permission.

A credit freeze will not prevent pre-screened offers from landing in your mailbox.

You have to lock each of your three credit reports separately

How do I Place a Credit Freeze on my Reports?

You may contact each credit bureau in writing or over the phone to request a credit freeze. However, the easiest and fastest way to request a freeze is over the web. Here’s how:

Equifax

To place a freeze, visit www.equifax.com/personal/credit-report-services/

Once there, you have to follow three simple steps to freeze your credit.

First, click on the “Get Started” button:

Then, enter your personal information, such as your name, date of birth, and social security number. Second, create an account. Lastly, verify your identity by answering a few security questions about items on your credit report:

Then, confirm that you want to place a freeze on your credit report:

After you click the button, you will choose which action you’d like to take in regards to a freeze on your credit. You can place a new freeze, or temporarily lift or remove an existing freeze from this page. Click next after you accept the terms and conditions:

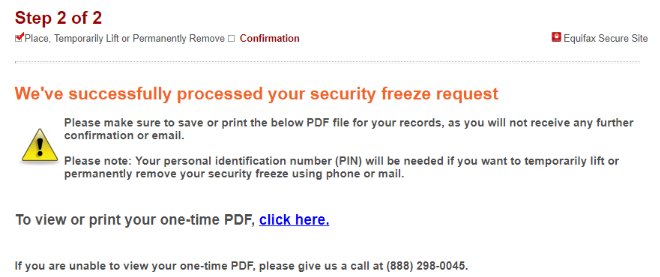

Then, hit the Submit button to process your request:

Once your credit has been frozen, you will be given a confirmation message and will have access to a PDF document with your PIN number:

This PIN number, which is randomly generated by Equifax, will be needed when you want to temporarily lift or permanently remove the credit freeze. Be sure to save it in a secure location.

Equifax has been pretty easy to deal with. I haven’t had any problems adding or removing a freeze from my Equifax credit report. They’ve made the process quite simple!

Transunion

To freeze your credit file with Transunion, visit www.transunion.com/credit-freeze

Once there, click on the “Add Freeze” button:

As you can see, you can also remove, or lift an existing freeze from this page, and you can add a credit freeze on behalf of your child and other family members.

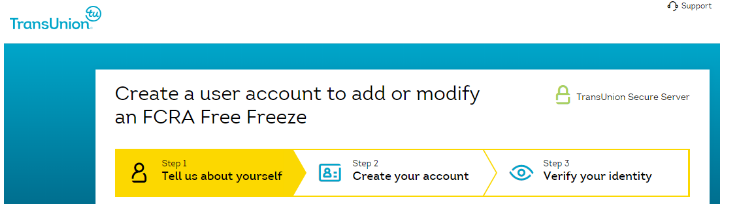

Once you click on the button, you’ll have to provide some personal information, such as your name, address and date of birth.

You’ll have to create an account. Then, verify your identity by answering questions about items that may be found on your credit report:

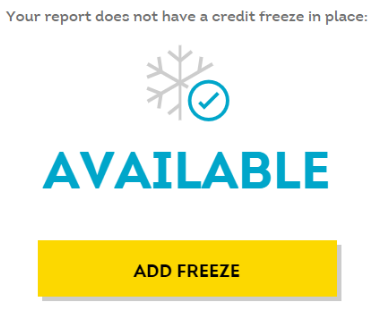

Based on the information you provide, Transunion will verify the status of your credit report and provide you with different available actions:

To continue with the process, after you click on the “Add Freeze” button, you’ll be asked to provide a PIN number. This PIN number will be used in the future when you want to lift or remove the freeze from your credit.

Once you’ve selected your PIN, you’ll be asked to confirm and submit your request.

Transunion has also made it very easy to manage a credit freeze online. I regularly lift my credit freeze temporarily if I know I’m going to need somebody to check my credit, and I’ve had no problem using Transunion’s system whatsoever.

Experian

To freeze your Experian report, visit www.experian.com/freeze/center.html

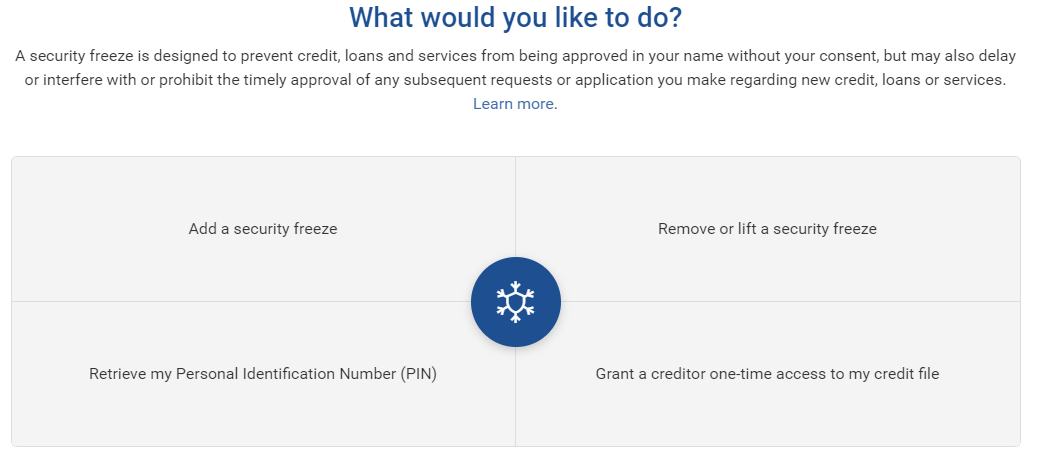

Once there, you’ll be given a variety of options:

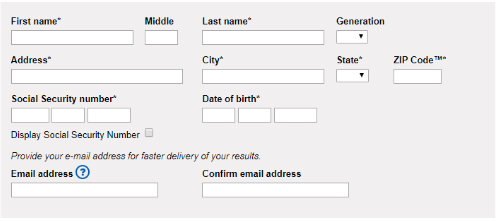

To add a security freeze, click on that square. You’ll be asked to provide some personal information:

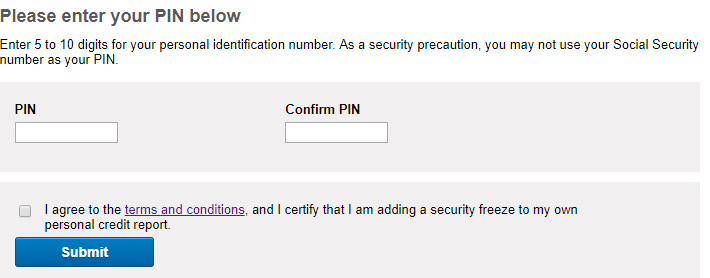

At the bottom of the page, you’ll be given the option to select your own PIN or have one assigned to you:

After you agree to the terms and conditions, hit the Submit button to freeze your credit.

To lift or remove an existing credit freeze, just visit the same web page again and select that option.

I have to say that Experian’s site has been by far the most difficult to deal with. When I first tried to add a security freeze, their website said that my file could not be located. I tried several times to no avail. Eventually, I was able to add a freeze through their automated phone line, 888-EXPERIAN.

However, when I needed to temporarily lift the security freeze, I ran into the same problem, and that phone number was no help.

When I tried contacting them, I couldn’t get to a live person for the life of me. I had to check online forums just to get a phone number that would help me connect with a human being.

In case you run into a similar problem and need to speak with a person at Experian, try calling 714-830-7000.

This brings me to my next point. A credit freeze is not for everybody.

Who is a Credit Freeze for?

If you suspect that you’ve been a victim of identity theft, or if you’re concerned that someone may use your information to open up new credit lines under your name, a credit freeze is a great way to protect yourself.

However, if you know that you’re going to have to use your credit soon, then a freeze may not be the best option for you.

Nowadays, it’s pretty common for landlords and even potential employers to check on your credit. If you know you’ll be moving or applying for a new job soon, be aware that you may have to lift any credit freeze you have beforehand.

As easy as it is to lift a freeze online, there may be issues like the one I encountered with Experian.

Are There any Alternatives to a Credit Freeze?

Yes!

If you don’t want to deal with the headache of lifting or removing a credit freeze every time you want to legitimately apply for credit, an alternative is to place a fraud alert on your credit instead.

What is a Fraud Alert?

A fraud alert is a notification you place on your report. It lets potential creditors know that they should take extra precautions to verify your identity when someone applies for credit using your information.

A potential creditor may try to contact you or ask you questions based on what they can see on your credit report to try and verify your identity before granting you credit.

How is an Alert Different from a Freeze?

You don’t need to add a fraud alert with each of the three credit bureaus. Instead, once you request for an alert with one of the bureaus, they must inform the other two bureaus so they can also place an alert on your credit file.

Placing an alert on your credit will also allow you to get a free credit report (not a credit score though) from each of the three bureaus for free once a year for as long as the alert is on your credit.

However, unlike a credit freeze, a fraud alert may still allow thieves to open new credit lines using your information if they manage to convince a potential creditor that they are you.

Although they can be renewed indefinitely, fraud alerts stay on your credit report for a year. Unlike a credit freeze which can be turned on or off at will.

Resources

Unfortunately, I’ve had to learn the hard way about identity theft. After my identity was stolen a couple times, I realized that identity theft is no joke.

If you’d like to learn more about how I took my credit score from the low 500’s to over 800, please check out my guide here.

I also recommend subscribing to a credit monitoring service such as myFICO. By checking your credit regularly, you can easily detect when anything’s wrong. The faster you act to protect your credit, the higher your chances of success.

Get started with myFICO here:

Final Thoughts

Data breaches are on the rise. A credit freeze or fraud alert are both great ways to protect your credit report from unauthorized use. For me, the thought of my data being available for thieves to use is a pretty scary thought.

How about you? Are you concerned about your data being out there? Please share in the comments below!

Another great way to protect your credit is to follow best practices for safeguarding your identity. You can also subscribe to a credit monitoring service. That way you can stay on top of any suspicious activity that may show up on your credit.

If you enjoyed this post, please share it!