Is the Most Effective Way to Avoid Overspending to Pay in Cash?

It may be inconvenient to pay in cash for items on a daily basis, but could this be the one thing that helps you stay within your budget? Read on to find out!

This post may contain affiliate links, which means I may earn a small commission at no extra cost to you. For more information, please see my disclosure here. Thank you for your support!

Have you ever been curious to “test” a statistic?

I’ve heard time and again that we tend to overspend when using credit cards, so I put this to the test and paid in cash for various spending for 3 months.

Here’s what I found.

From automating payments from your bank account to paying with your phone, as we move closer to becoming a cashless society, I started to wonder what effect, if any, using cash or credit could have on spending habits.

According to Psychology Today, credit cards or other forms of cashless payment methods, make you spend more for a variety of reasons.

Spending and Our Brains

When we pay with cash, which is tangible, we tend to feel the weight of what we’re purchasing.

On the other hand according to the Psychology Today article, paying with credit minimizes the ‘pain of paying’ for that purchase.

Why?

Because it delays the actual payment.

Not only that, but it allows consumers to combine their purchases throughout the billing cycle and make a bulk payment later.

In other words, by the time you pay your credit card bill every month, you probably don’t remember every single $5 purchase that makes up your balance for that particular billing cycle.

This helps mask your spending habits if you’re not paying close attention to them.

Additionally, since credit cards reduce the pain of our purchases, the article notes that we tend to make better decisions when paying with cash.

This reduces the overall amount of spending on impulse purchases.

The Pay in Cash Switch

After reading this, and several similar articles, in December of 2016 I decided to exclusively pay in cash for any discretionary, or flexible, spending that I figured would be easy to switch to cash payments.

I chose groceries, dining out, entertainment, and other shopping.

This would be anything like clothes, school supplies, kitchen and home items, pet supplies, etc.

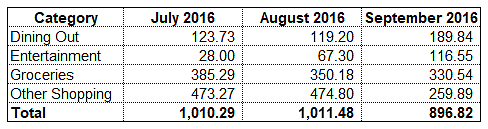

Here’s how much I spent on those expenses on credit:

After a little over a year of paying exclusively with cash in these categories, I went back and looked at my spending before and after I made the switch.

For comparison purposes, I chose to compare three months of spending year over year to ensure that there wasn’t anything crazy going on in any one particular month.

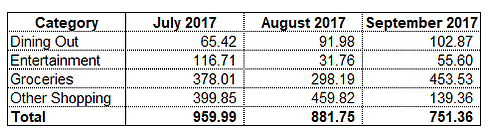

Here’s my expenses in those same categories after I switched to exclusively paying cash:

Related Posts

Insomnia Can Derail Your Finances. Here’s How to Keep Them on Track

How to Get Out of Debt by Changing this One Simple Habit

5 Amazing Tools to Rule Your Money This Year

The Results

I was stunned to see the results.

On the months of July, my total savings were $50.30, or 5%.

On my second month, August, my savings were $129.73 or 13% of my baseline month.

By the third month, I saved a total of $145.46 or 16% of my original expenses.

Do you want to learn more about my fail-safe budgeting technique? Download my Free Quick Start Guide to Budgeting. Learn how I was able to quickly revamp my finances and consistently save money every single month!

Is it Worth it?

Although it may not sound like big dollars, just by switching to paying cash for these four types of expenses, I managed to save a total of $325.49 in three months.

That’s over $100 a month that my budget could certainly use.

Additionally, by switching to paying in cash for more and more expenses, I’ve been able to save much more in the past few months.

When I started to pay in cash for variable spending, I started taking out $800 a month from the bank, but I can now manage to comfortably get by with only $500 or so a month in cash.

Those are an additional $300 that I can save up or invest, and that’s definitely worth it!

Recommendations

I do have to say that I don’t necessarily enjoy dealing with cash.

Here’s how I was able to stick with it.

Use the Cash Envelope System

For the first several months while I got used to this new system, I found it useful to use a multi-colored cash envelope system.

It allowed me to quickly locate the spending category I was looking for without having to fumble in my purse for long. You can get yours here:

Use an App to Track Your Spending

As I mastered the envelope system and became more comfortable handling cash though, I switched systems.

What worked best for me was using a spending tracking app that would allow me to set different categories.

This way, I can see my spending at a glance with various charts and visuals on the go.

This helped me make decisions on the spot as to whether or not I have enough money left on a particular category in my budget for the month.

I really enjoy the Spending Tracker App, which I have for iPhone.

If you have an Android, there’s plenty of spending tracking apps also available for Android here.

Adjust How Much You Pay in Cash

I also recommend setting a specified amount of cash you’d like to designate for variable expenses, and reduce it gradually every couple of months.

When I first switched to paying with cash, I kept running out of money.

By the fourth month though, I was consistently ending the month with extra money, so I started reducing the amount of cash I’d withdraw from the bank.

Once I started having extra money again, I lowered down my withdrawal amount even more.

The key is to prepare your brain to know that once the cash is gone, spending for the month is over.

Avoid the temptation of just using a card if you’ve ran out of money.

Personally, it took me a couple of months to master this, but I definitely recommend it.

Do you want to learn more about my fail-safe budgeting technique? Don’t forget to download my Free Quick Start Guide to Budgeting here!

Are there any expenses you always pay in cash for? Join the conversation below!